Intax Presents

Budget 2022

OVERVIEW

Budget 2022 was announced on Tuesday, 13 October 2021.

This document sets out the main changes in taxation, social welfare, health, housing, education, employment and other areas.

It is an overview and not a complete statement of the measures announced in Budget 2022.

There might be updations to the budget in the future.

Some of the changes announced in the Budget come into effect immediately. Others take effect from the beginning of January 2022 or later in 2022. Many others have to be finalised before coming into effect.

Some elements of these measures may change when the legislation required to bring them into effect is enacted.

LOOKING TO FILE YOUR TAX RETURN/ FORM 11?

Apply now to www.taxreturned.ie & Get a FREETax Assessment

Wage Supports

The Employment Wage Subsidy Scheme (EWSS), which was due to expire in December 2021, has been extended to 30 April 2022. The payment levels will begin to be tapered from December 2021 and the scheme will be closed to new applicants from 1 January 2022.

Warehousing of Tax Liabilities. The Tax Debt Warehousing Scheme is expanded to allow self-assessed income taxpayers with employment income who have a material interest in their employer company to warehouse income tax liabilities relating to their Schedule E income from that employer company.

Remote Working

Remote workers can claim tax relief on 30% of vouched heating and electricity expenses for the days they are working from home. This is an increase from the current limit of 10%. The temporary concession for broadband expenses, whereby 30% of the cost can be claimed back, has been made permanent.

Employment Investment Incentive Scheme

The Employment Investment Incentive (EII) Scheme is extended for three years to December 2024. The scheme is a tax incentive that allows an individual investor to obtain income tax relief of up to 40% on investments for shares in certain companies.

The EII Scheme is being opened up to a wider range of investment funds and the rule that 30% of an investment in an EII company must be spent before relief can be claimed is removed.

To allow greater capacity for investors to redeem their capital without penalty, the ‘capital redemption window’ rules are being relaxed.

Help to Buy Incentive

The Help to Buy incentive is a scheme for first-time buyers. Budget 2022 extends the scheme to December 2022. There have been no changes to the rates of the scheme, which still offers first-time buyers a tax rebate of up to €30,000 or 10% of the purchase price of the property. A full review of the scheme will be carried out in 2022.

Zoned Land Tax

A new self-assessed zoned land tax, replacing the Vacant Site Levy, will be introduced to encourage the use of land for building homes. The tax will apply to land that is zoned as suitable for residential development and is serviced but has not been developed for housing. The tax will be 3% of the market value of the land.

There will be a number of exclusions from the tax, and a lead time of at least 2 years before the tax is applied(commencing in 2024).

Pre-letting Expenses for Landlords

The relief for certain pre-letting expenses of landlords on vacant residential premises, which is capped at €5,000 per premises, will be extended for a further 3 years to the end of 2024.

Corporation Tax

A new tax credit for the digital gaming sector is introduced by providing a refundable corporation tax credit for expenditure incurred on the design, production and testing of a digital game. The relief will be available at a rate of 32% on eligible expenditure up to a maximum of €25 million per project and there will also be a per-project minimum spend requirement of €100,000.

The relief for certain start-up companies from corporation tax is extended for a period of 5 years until 31 December 2026.

The accelerated capital allowance scheme for energy-efficient equipment, which allows the full cost of expenditure on qualifying energy-efficient equipment to be deducted for tax purposes in the year of purchase, has been amended so that equipment directly operated by fossil fuels no longer qualifies for the scheme.

The accelerated capital allowance scheme for gas vehicles and refuelling equipment, which allows an accelerated deduction when businesses invest in vehicles powered by natural gas/biogas and related refuelling equipment, is extended to December 2024 and is amended to include hydrogen-powered vehicles and refuelling equipment.

International Corporation Tax Reform

The Irish Government has signed up to OECD proposals for a global minimum effective corporation tax rate of 15% for multinationals with global revenues in excess of €750 million.

Ireland has negotiated an effective minimum rate set at 15% instead of the original “at least 15%” proposal by the OECD and endorsed by the G7 earlier this year. Ireland has also secured agreement that the 12.5% rate will continue to apply to companies below the €750 million revenue threshold. The new rules are expected to be implemented as early as 2023.

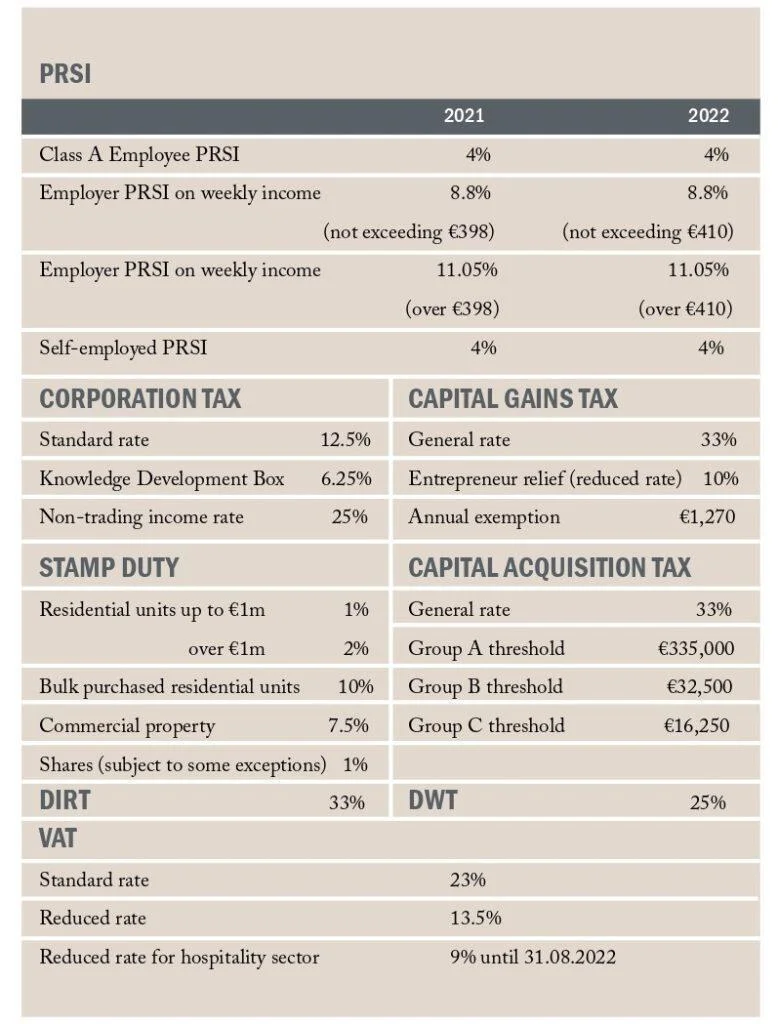

VAT The reduced VAT rate of 9% for the hospitality sector will remain in place until 31 August 2022.

Commercial Rates

The commercial rates waiver will continue until 31 December 2021. The waiver of commercial rates was originally introduced as a COVID-19 emergency support measure in March 2020. The waiver applies to the hospitality, arts and tourism-related sectors.

Carbon Tax

In a drive to further decarbonise the economy and meet Ireland’s commitment to reduce carbon emissions by 7% in 2022, the rate of carbon tax on fuels will increase again this year by €7.50 per tonne/ CO2. Carbon tax will rise by the same amount in every Budget until 2029, further increasing the cost of petrol, diesel and home-heating fuels.

Income from Micro-generation of Electricity

A tax disregard of €200 is being introduced for personal income received by households that sell any residual electricity they generate back to the grid.

Vehicle Registration Tax and Electric Vehicles

Budget 2022 amends Vehicle Registration Tax (VRT) rates to further encourage the transition to lower-emission fuels.

From January 2022, a revised VRT table will be introduced. The 20-band table will remain; however, there will be a 1% increase for vehicles that fall between bands 9-12, a 2% increase for bands 13–15, and a 4% increase for bands 16–20.

The €5,000 relief from VRT for battery electric vehicles (BEVs) is extended to the end of 2023.

The BIK exemption where an employer makes a BEV (both new and used) available to employees has been extended until 2025. This exemption was due to end on 31 December 2022.

Agri Tax Measures

The Young Trained Farmer Stamp Duty Relief is extended to December 2022. This measure provides relief from stamp duty on the conveyance of farmland to eligible young trained farmers.

Stock relief is extended for a further 3 years to December 2024. This relief provides for stock relief at a rate of 25% of the amount by which the value of farm trading stock at the end of an accounting period exceeds the value of farm trading stock at the beginning of the same accounting period.

Enhanced Stock Relief for young, trained farmers and for registered farm partnerships is also extended for 1 year to December 2022.

The Farmers Flat Rate Addition is decreased from 5.6% to 5.5%. The flat-rate scheme compensates unregistered farmers for VAT incurred on their farming inputs.

Bank Levy

The bank levy, which was due to expire in 2021, is being extended for one further year to December 2022.

WE PROVIDE IRISH TAX AND BUSINESS SERVICES

Accounting, taxation, Business Set-up & contracting services

Umbrella Company Services

Copyright © 2021 taxreturned.ie, All rights reserved